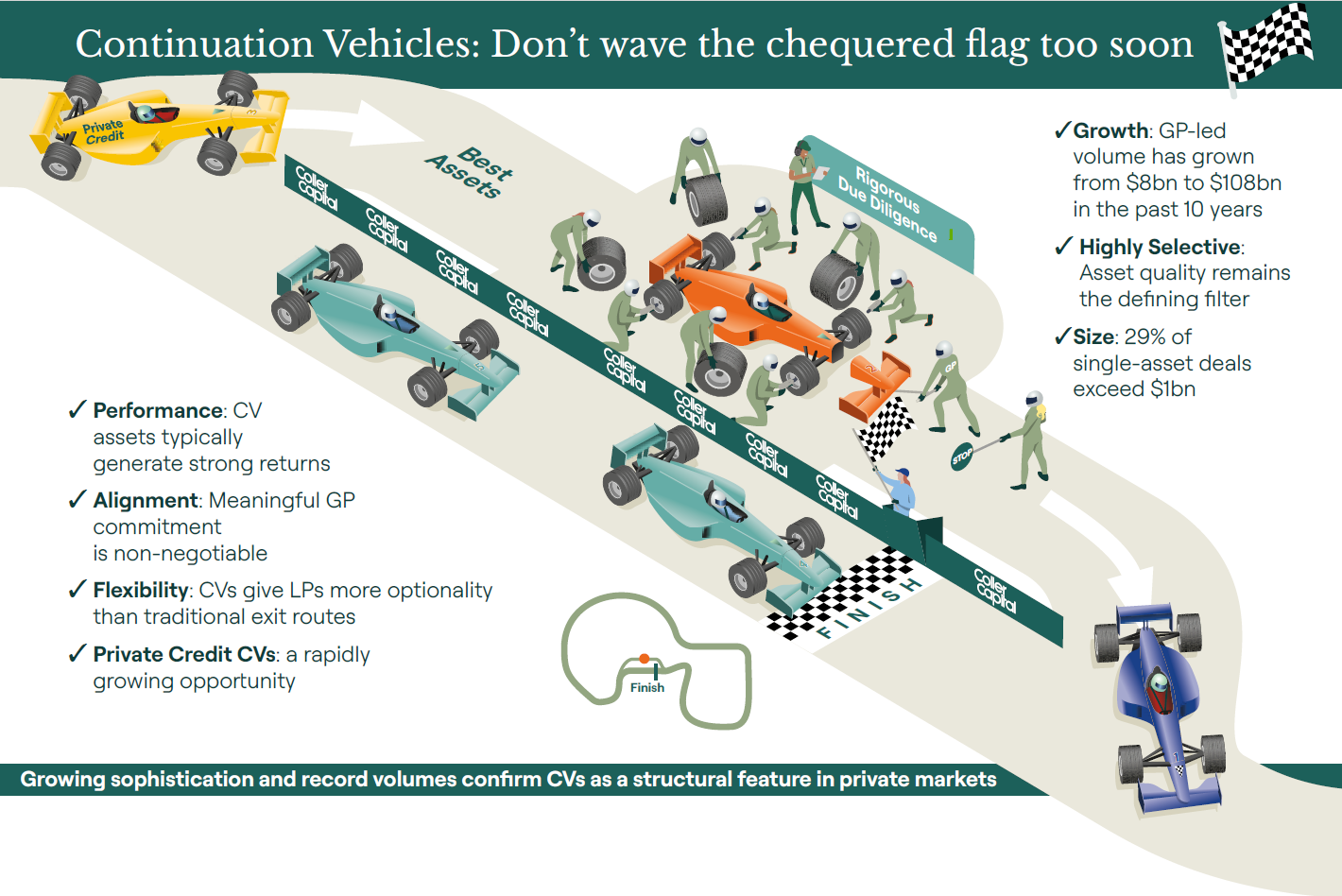

Record volumes and growing sophistication confirm continuation vehicles as a structural feature of private markets

GP-led transaction volumes hit a record $108 billion in 2025, up from $77 billion in 2024 and more than 13x the $8 billion recorded a decade ago¹. Single-asset continuation vehicles are now the most prevalent transaction format, with 29% of deals now exceeding $1 billion¹. The secondary market is structurally underfunded relative to primary private capital, with just one year of dry powder, giving investors significant selectivity to ensure the quality of their investment decision making remains high.

00:00:05 – 00:00:14

I think the biggest change in GP-leds that have made them mainstream, is firstly LP acceptance that many deals are happening these days.

00:00:14 – 00:00:20

LPs are seeing them all the time and they recognise they’re a good form of liquidity.

00:00:20 – 00:00:30

I think also ILPA guidance has been important in terms of setting a framework for how transactions should be executed. And I think finally, maybe I’d say just capital formation.

00:00:30 – 00:00:39

A lot of capital has been raised for these transactions, and I think those three elements together make GP-leds front and centre for LPs now.

00:00:39 – 00:01:14

The biggest change in terms of acceptance of GP-led transactions has been LP’s acceptance in terms of this as a liquidity methodology.

00:01:14 – 00:01:21

I think one change is that certainly LP acceptance has moved on significantly. Given the volume of these transactions.

00:01:21 – 00:01:31

So that’s the first thing I would say. The second thing I would say is capital formation around GP’s is being materially over the last few years. So there is capital available for these.

00:01:31 – 00:01:38

And maybe third, the guidance around GP transactions is very clear.

00:01:38 – 00:01:48

So if that is followed with LP acceptance and with capital, I think we have a structural change in the market, which has really changed the game for GP lens.

00:01:48 – 00:02:00

I think the biggest change in GP leds that have made them mainstream is firstly LP acceptance that many deals are happening these days.

00:01:58 – 00:02:04

LPs are seeing them all the time and they recognise they’re a good form of liquidity.

00:02:04 – 00:02:14

I think also LP guidance has been important in terms of setting a framework for how transactions should be executed, and I think finally, maybe I’d say just capital formation.

00:02:14 – 00:02:23

A lot of capital have been raised for these transactions. I think those three elements together make GP led front and centre for LPs now.

00:02:23 – 00:02:33

The biggest change in terms of acceptance of GP led transactions has been LP’s acceptance in terms of this as a liquidity methodology.

Continuation vehicles have become what Nigel Dawn of Evercore describes as ‘the third door of liquidity‘ for GPs, alongside M&A and IPOs². Rather than being forced by fund timelines to sell high-performing assets to competitors, GPs can transfer those assets into a new vehicle, maintain control, and pursue the next stage of value creation — while offering existing LPs a genuine choice: exit at fair value, or roll forward and capture further upside.

1 Paul Lanna, Coller Capital. (2026, April). “GP-Led Continuation Funds Panel”, Coller Capital LP Meeting.

2 Nigel Dawn, Evercore. (2026, April). “GP-Led Continuation Funds Panel”, Coller Capital LP Meeting.