Liquidity and secondaries

GPs face a range of LP views on exit timings, while investors see continuation vehicles as an established feature of private markets.

As private equity holding periods continue to lengthen, liquidity remains a priority for many GPs. Yet LPs often have differing investment horizons, which can make the decision of whether to sell or give companies more time for value creation a difficult balancing act.

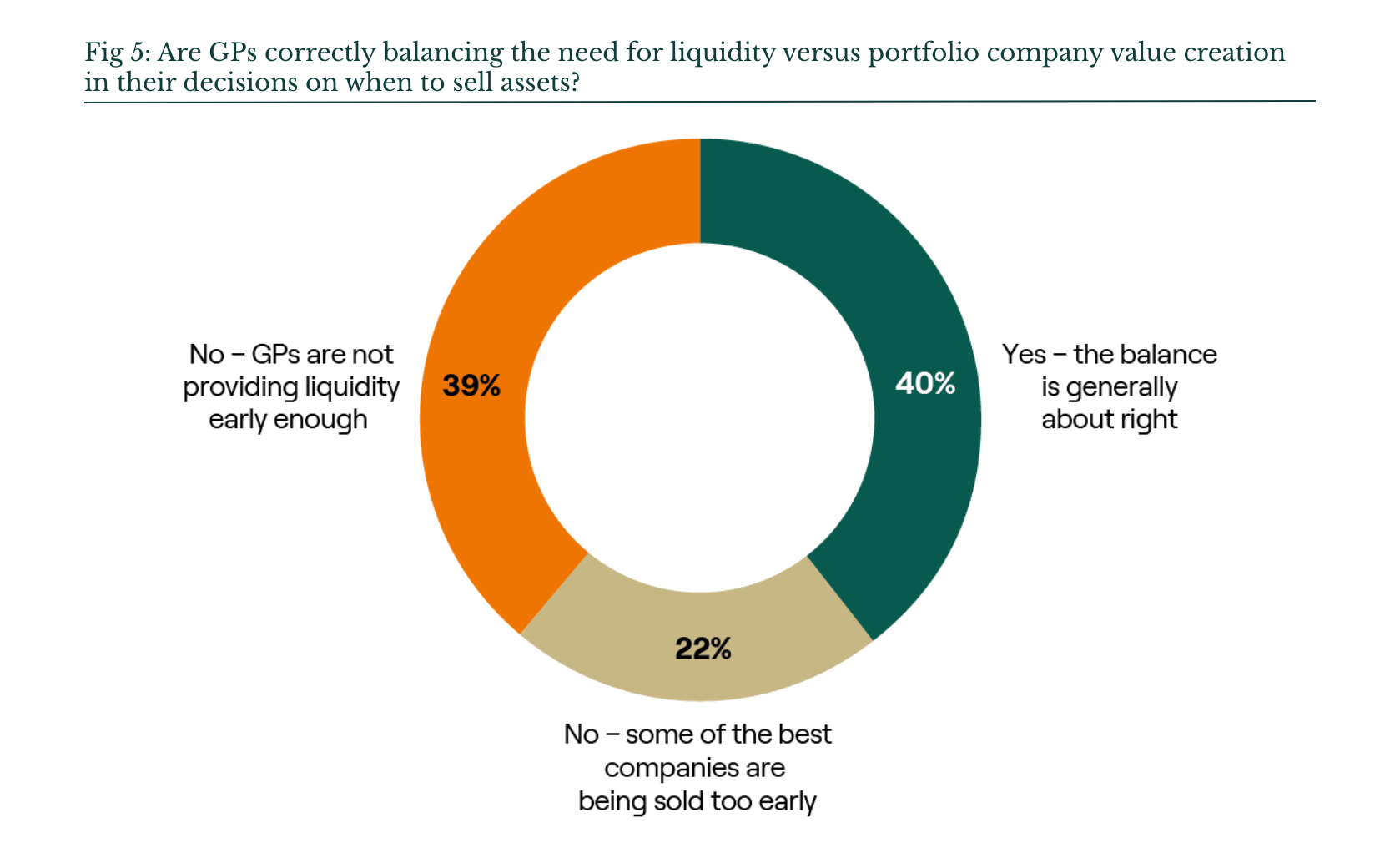

Our survey clearly illustrates this. When asked whether GPs are correctly balancing liquidity needs and potential portfolio company value, the encouraging news is that 40% of LPs believe that they are getting it right. However, the same proportion say that GPs are not providing liquidity early enough, and a further 22% say the best companies are being sold too early.

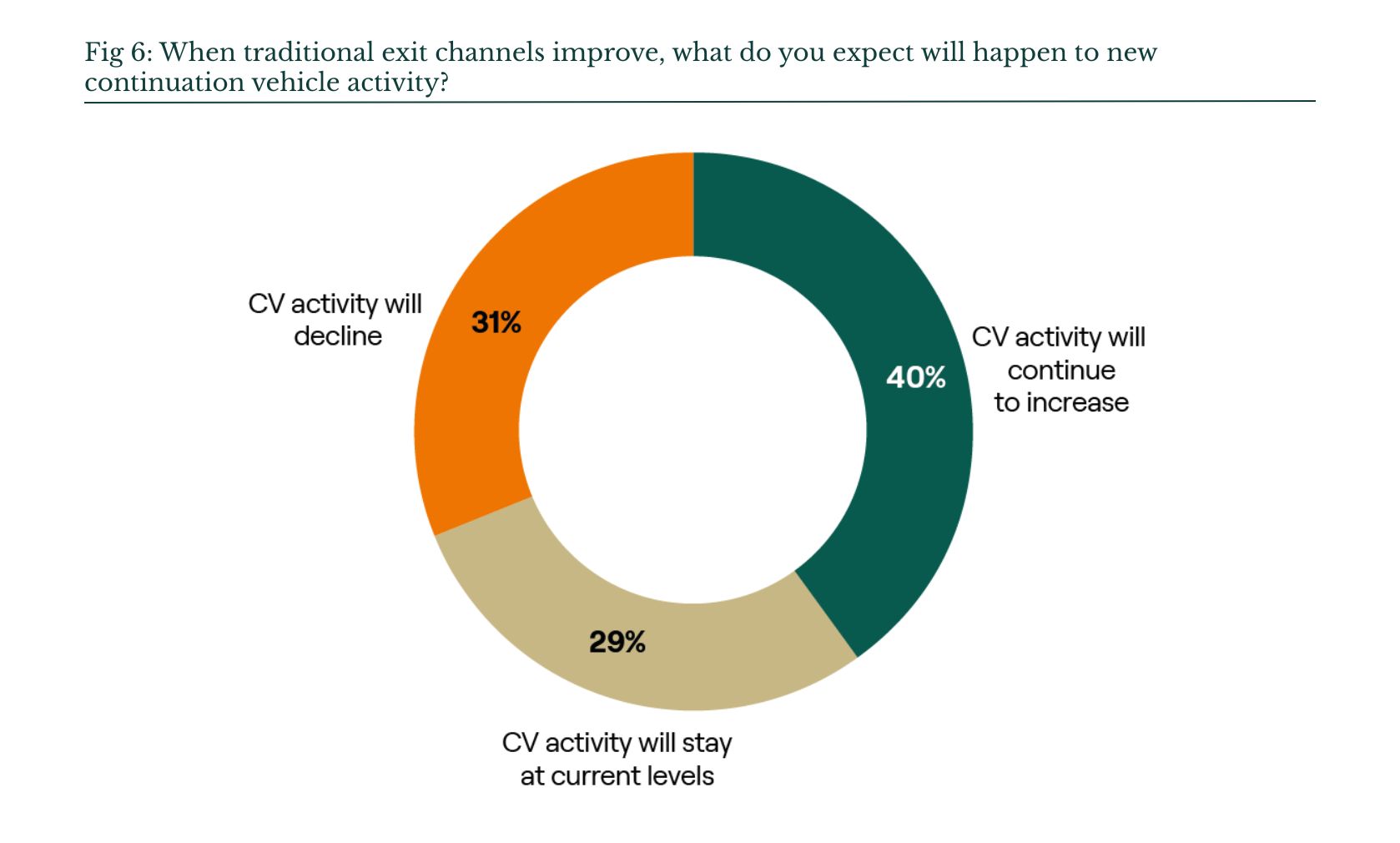

By offering LPs the option of selling for liquidity or rolling to retain their investment, continuation vehicles (CVs) can offer a solution to conflicting investor holding period expectations. Following rapid growth in recent years, these transactions appear to have gained acceptance among LPs as an established feature of private markets. Even when exit conditions improve, 40% expect CV activity to continue increasing, 29% anticipate it will stay at current levels and just under a third (31%) say it will decline.

00:00:05 – 00:00:11

Two findings from the latest Barometer on how LPs are thinking about exits.

00:00:11 – 00:00:16

First, what LPs agree on. Continuation vehicles are here to stay.

00:00:16 – 00:00:24

Even when traditional exit channels recover, 40% of LPs expect CV activity to keep growing.

00:00:24 – 00:00:31

29% expect it to hold steady, while 31% expect it to decline.

00:00:31 – 00:00:35

The cyclical workaround label doesn’t fit anymore.

00:00:35 – 00:00:41

LPs see continuation vehicles as a permanent feature of private markets.

00:00:41 – 00:00:48

Where LPs differ is on the timing of the exit itself and this is the harder problem for GPs.

00:00:48 – 00:00:59

Just 40% of investors think managers are getting the balance right. While the same numbers say GPs aren’t providing liquidity early enough.

00:00:59 – 00:01:10

The remaining 22% say the best companies are being sold too soon. Endowments and foundations are the most likely to want GPs to hold longer.

00:01:10 – 00:01:23

So the same exit decision, on the same asset, can leave one LP frustrated they didn’t get cash sooner – and another frustrated the company didn’t get more runway.

00:01:23 – 00:01:30

That’s the tension GPs are navigating. No exit decision will please all investors.

00:01:30 – 00:01:40

This is part of the reason why continuation vehicles have become so attractive. They help GPs solve for differing objectives.

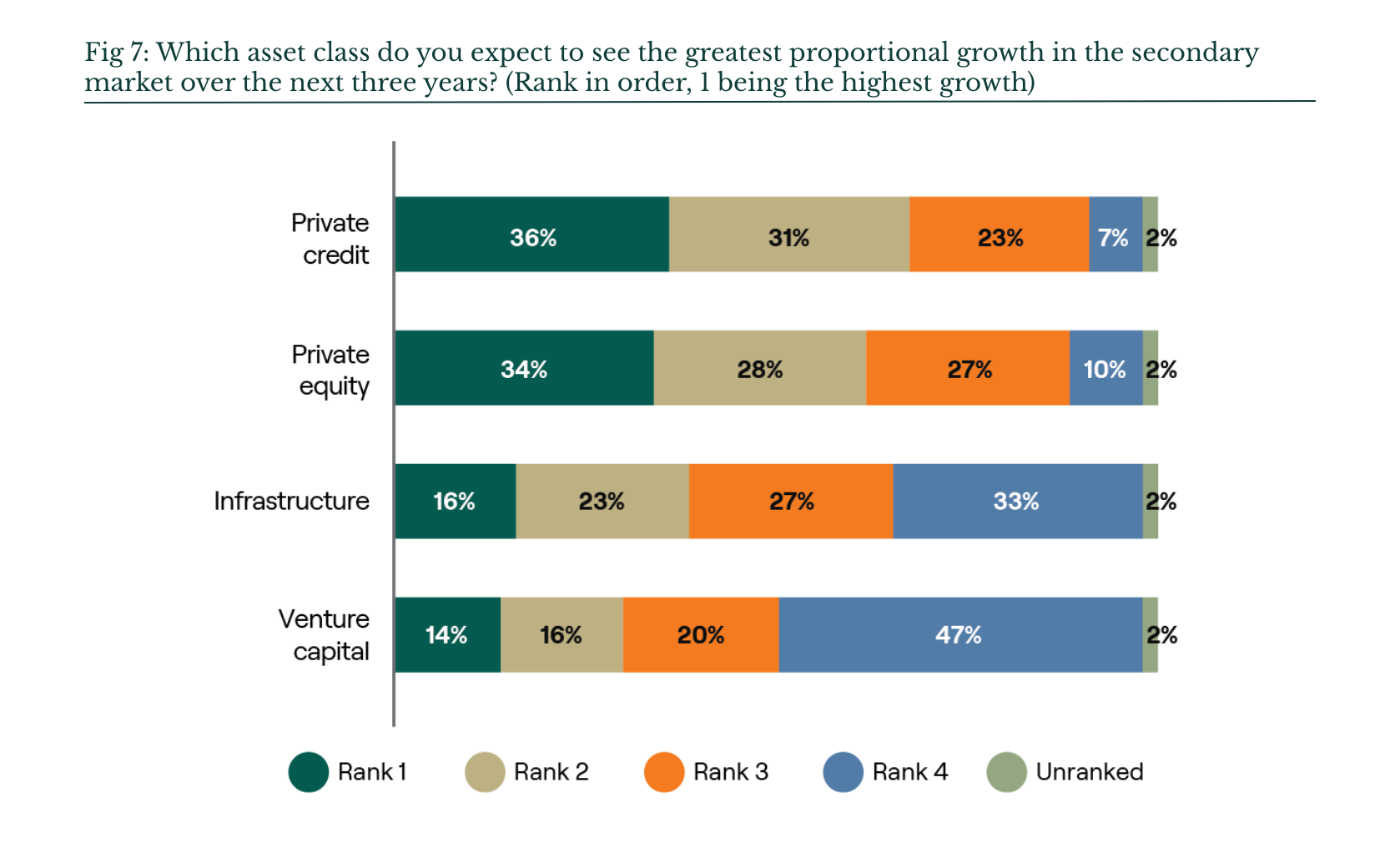

With LPs seeking liquidity and managing their portfolios more actively, secondaries transaction volume has increased substantially in recent years across all private markets asset types. Of these, LPs expect private credit secondaries to see the greatest proportional growth in the next three years. Primary private credit’s considerable expansion in recent years is undoubtedly increasing deal flow and portfolio rebalancing is also likely a driver.