Allocation decisions

LPs continue to deploy capital in an uncertain environment, but geopolitics have become a bigger factor for some investors’ allocation decisions.

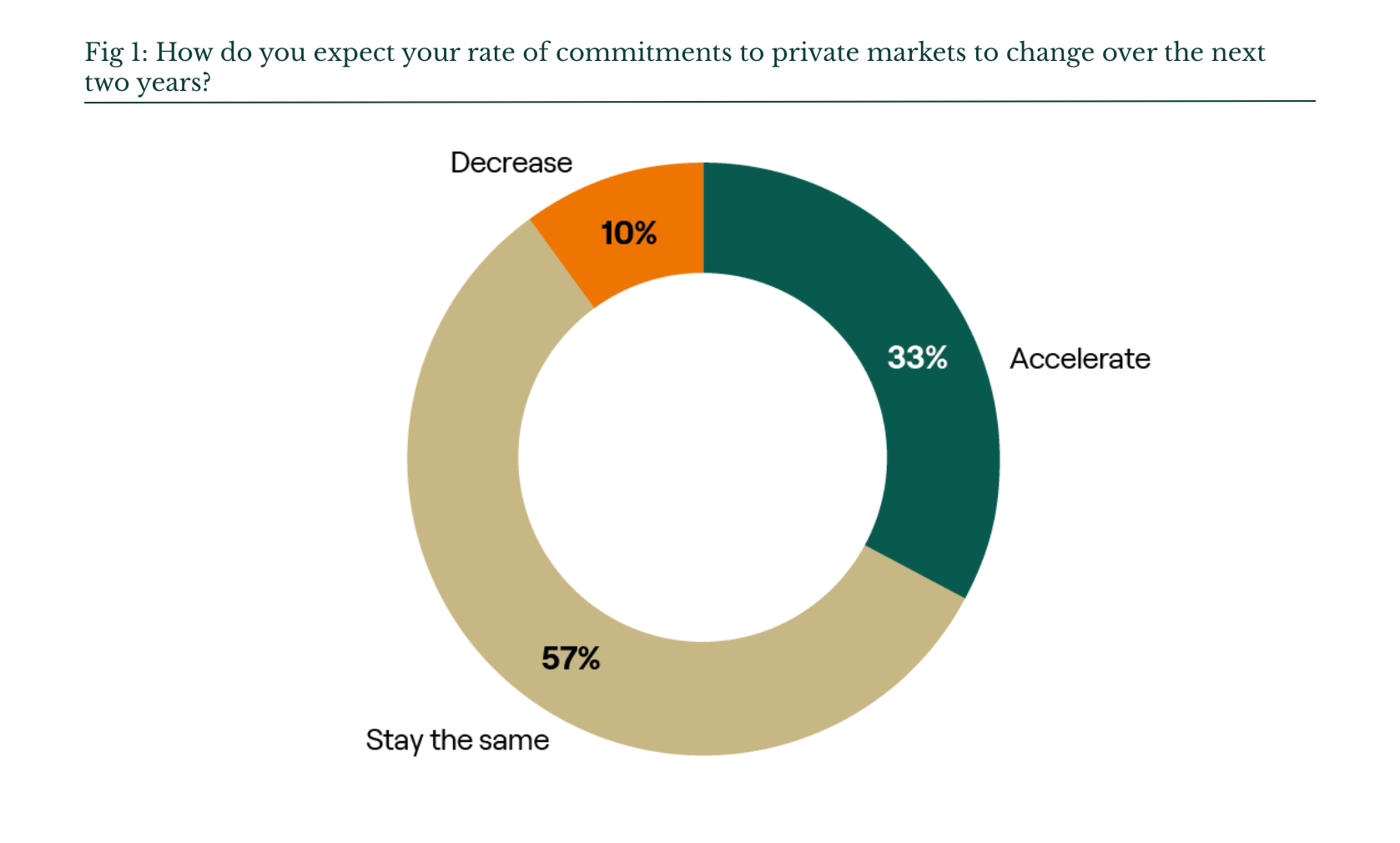

As an asset class with long-term investment horizons, private markets can often insulate LP portfolios from the effects of short-term shocks. It is therefore unsurprising that LPs are continuing to deploy capital in private markets even as world events take an unpredictable turn. A third expect to accelerate their commitment pace in the next two years while 57% expect it to remain the same.

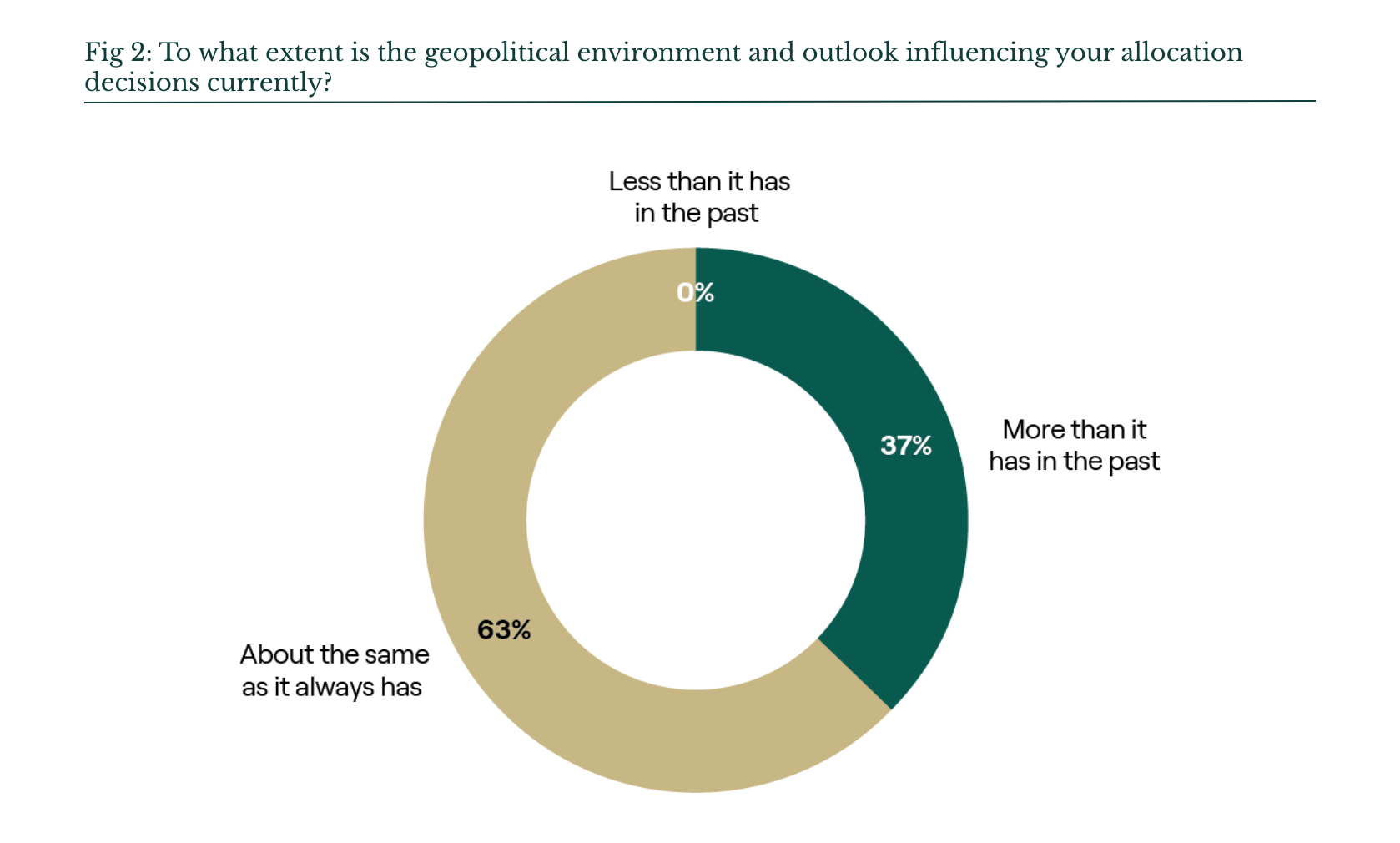

Indeed, on the face of it, LPs appear sanguine about geopolitics when making allocation decisions. Nearly two-thirds (63%) of respondents overall say there is no change to how much the geopolitical environment and outlook are influencing their current allocation decisions. With no respondents saying it has less bearing than it has had in the past, that leaves just over a third (37%) who say it is influencing their decisions more than in the past.

However, closer examination paints a more mixed picture. Among our North American respondents, just under a quarter (23%) consider geopolitics more than previously. By contrast, other regions appear more concerned: nearly half of respondents elsewhere are giving geopolitics more weight when allocating.

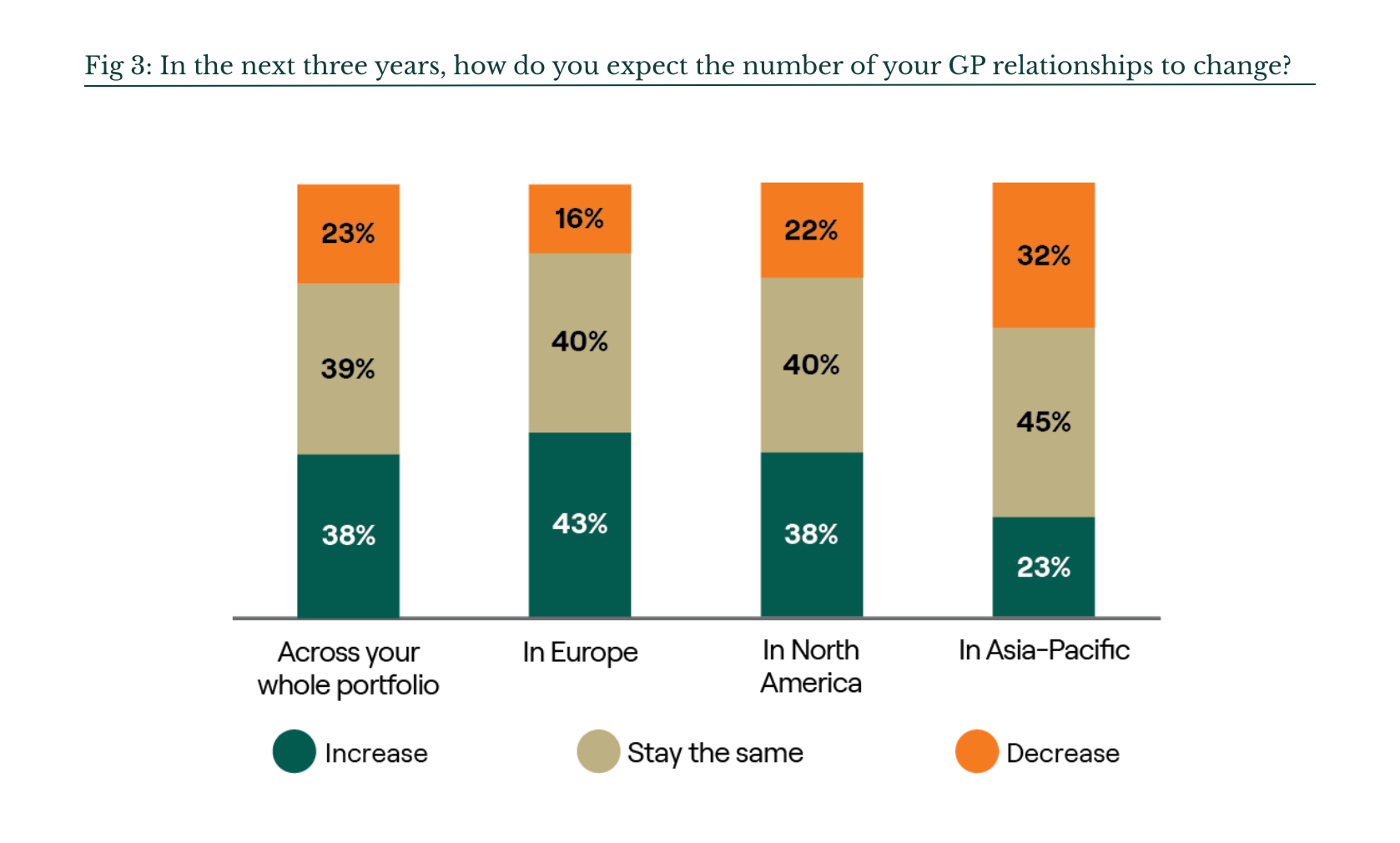

More LPs (23%) expect to reduce the number of GP relationships in their portfolios than in the past. This is a shift from the last time we asked this question – in 2020 – when just 16% were expecting to reduce GP relationship numbers. On the flip-side, just over a third (38%) of respondents anticipate an increase across their whole portfolio.

00:00:06 – 00:00:12

Ask an LP today whether geopolitics is changing how they allocate to private markets.

00:00:12 – 00:00:16

The answer may depend considerably on where they’re sitting.

00:00:16 – 00:00:29

In our Summer 2026 Barometer, 47% of LPs in Asia Pacific say geopolitics is influencing allocation decisions more than in the past.

00:00:29 – 00:00:37

In Europe, 46%. In North America, it’s just 23%, roughly half the rate.

00:00:37 – 00:00:39

That gap matters.

00:00:39 – 00:00:50

If you’re a GP fundraising in Singapore, Frankfurt or Dubai, country exposure, supply chain resilience and trade policies aren’t side questions.

00:00:50 – 00:00:58

They are front-and-centre considerations. In California, these considerations might be of second order.

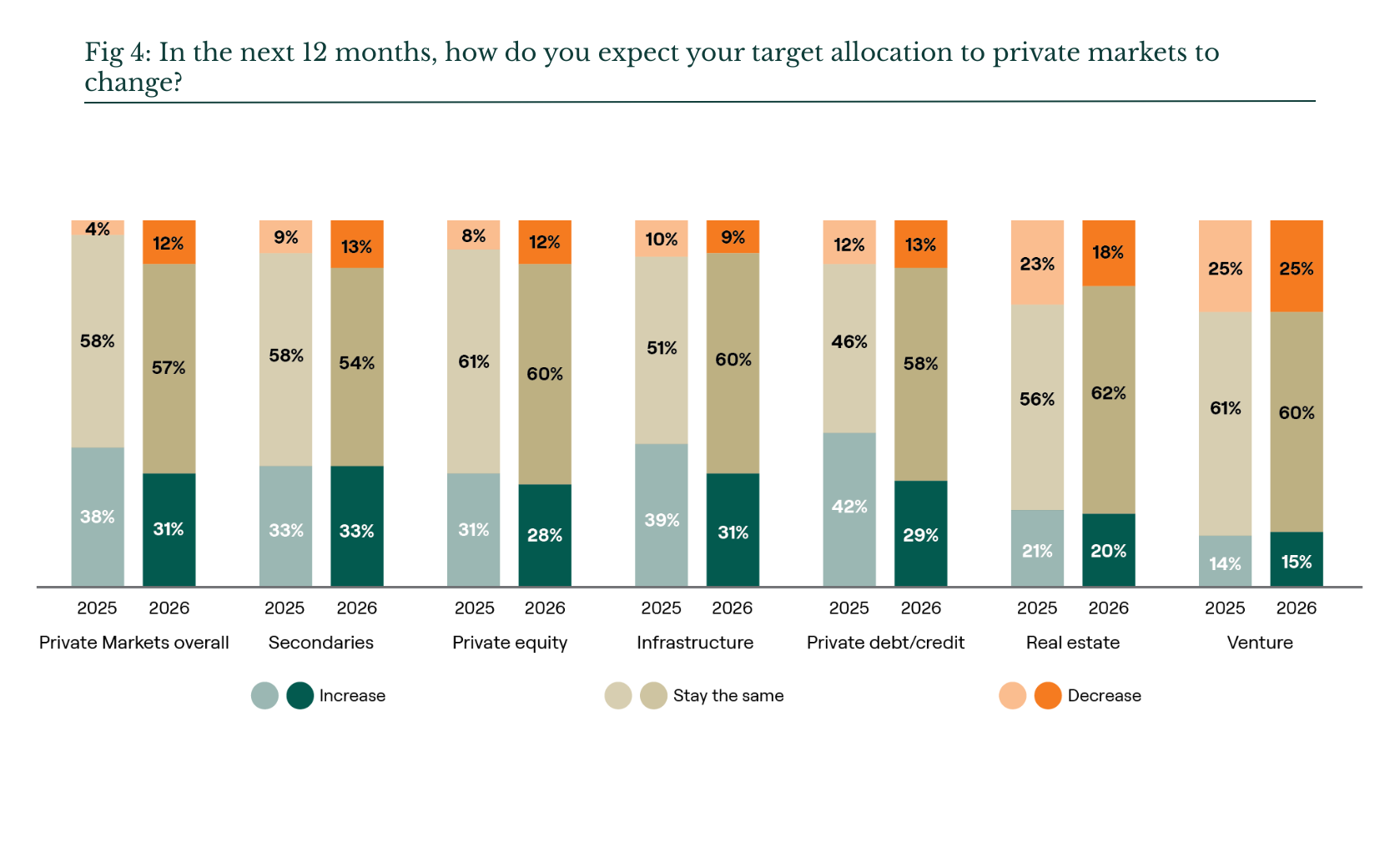

While most (57%) respondents expect no change to target allocations overall LPs have cooled on private credit and infrastructure when compared to our last Barometer six months ago when 42% expected to increase target allocations to private credit versus this time when just 29% say the same. In infrastructure, the proportion has fallen from 39% to 31% over the same period.

This may be a natural pause following periods of rapid growth for both asset types, yet recent negative headlines regarding private credit are also likely influencing LPs’ allocation plans. Despite this, it’s worth noting that the vast majority of investors (88%) still expect to maintain or increase private credit allocation targets in the next 12 months.

00:00:05 – 00:00:10

Private credit isn’t falling out of favour. But it is having a moment of pause.

00:00:10 – 00:00:30

In the latest Coller Capital Barometer, the proportion of LPs planning to increase private credit allocations over the next 12 months has fallen from 42% in our Winter 2025-26 Barometer to 29% in just six months.

00:00:31 – 00:00:37

Infrastructure has seen a similar drop from 39% to 31%.

00:00:37 – 00:00:43

Two of the fastest-growing asset classes in private markets, both cooling at the same time.

00:00:44 – 00:00:55

But the important context here is that 87% of LPs still plan to maintain or increase private credit allocations.

00:00:55 – 00:01:02

But capital is being deployed more carefully. And there’s another signal that came through in the data.

00:01:02 – 00:01:11

When LPs were asked which asset class will see the greatest proportional growth in the secondary market over the next three years?

00:01:11 – 00:01:14

Private credit topped the list.

00:01:14 – 00:01:28

36% ranked it first, just ahead of private equity. So even as primary allocation enthusiasm cools, LPs are expecting a lot more activity in private credit secondaries.

00:01:28 – 00:01:33

This points to a market maturing, not retreating.

00:01:33 – 00:01:44

Primary commitments are being made with more discipline. And the secondaries market is playing an important role in facilitating liquidity.