By the numbers

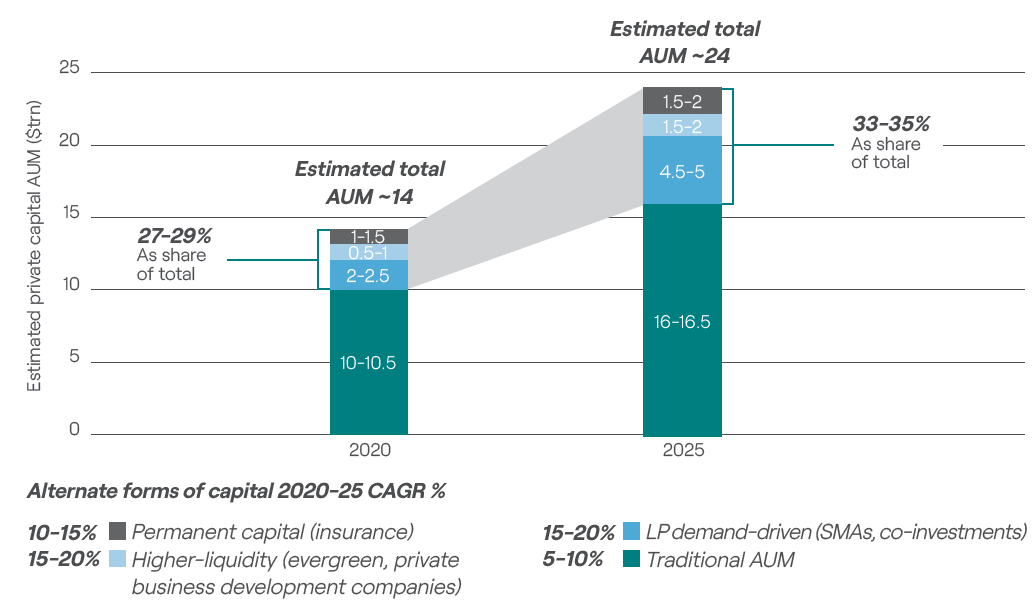

Private markets AUM growth shifts outside traditional funds.

Private markets have continued to grow AUM at pace — despite challenging fundraising – largely by attracting capital for structures other than closed-end funds, such as evergreens and co-investments.

Closed-end fund AUM had an estimated compound annual growth rate (CAGR) of between 5% and 10% from 2020 to 2025, according to McKinsey & Company’s Global Private Markets Report 2026. However, the rate for evergreen, co-investment and separately managed accounts (SMAs) was higher, at 15% to 20%.

Permanent capital (insurance balance sheet capital and perpetual life companies) also grew faster than closed-end AUM, with an estimated CAGR of 10% to 15% in the same period. Estimates are based on private capital AUM reported by GPs.

Non-traditional AUM now accounts for at least a third of private capital AUM, up from around 28% in 2020.

Source: CEM Benchmarking; Cerulli; Kohlberg Kravis Roberts; Preqin; Sovereign Wealth Fund Institute; StepStone; McKinsey analysis

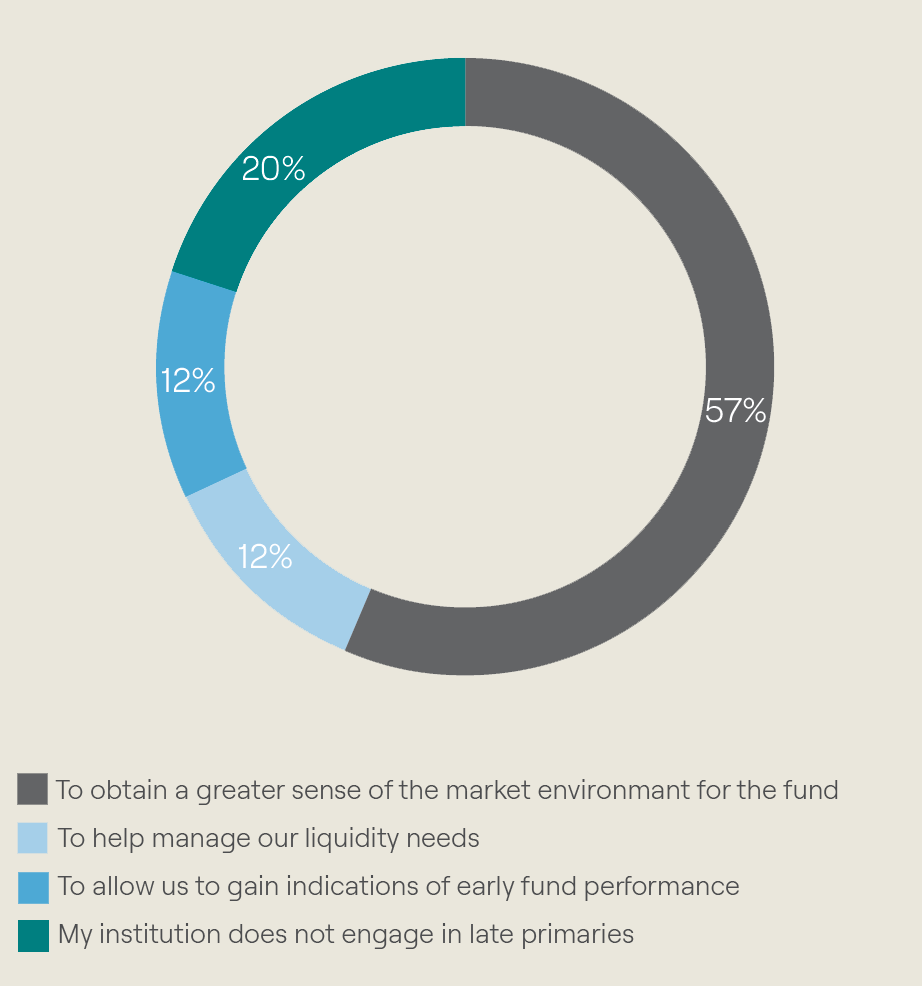

Late primaries on the rise

If you expect your institution to engage in more late primaries, what will be the main reason?

As fundraising periods stretch, many limited partners are holding out for evidence on funds’ early performance before committing, according to Coller Capital’s Global Private Capital Barometer, Winter 2025-26.

As fundraising periods stretch, many limited partners are holding out for evidence on funds’ early performance before committing, according to Coller Capital’s Global Private Capital Barometer, Winter 2025-26.

Around four-fifths of LPs engage in late primaries – commitments to funds that are still raising but that have already deployed significant capital into portfolio companies. Over half (57%) do so mainly to gauge early fund performance, while understanding the market environment and managing liquidity is the main motivation for 12% apiece.

Nearly a quarter (24%) expect to engage in more late primaries than two years ago, 59% plan to maintain the same level, and just 5% anticipate doing fewer.

Source: Coller Capital, Global Private Capital Barometer, Winter 2025-26

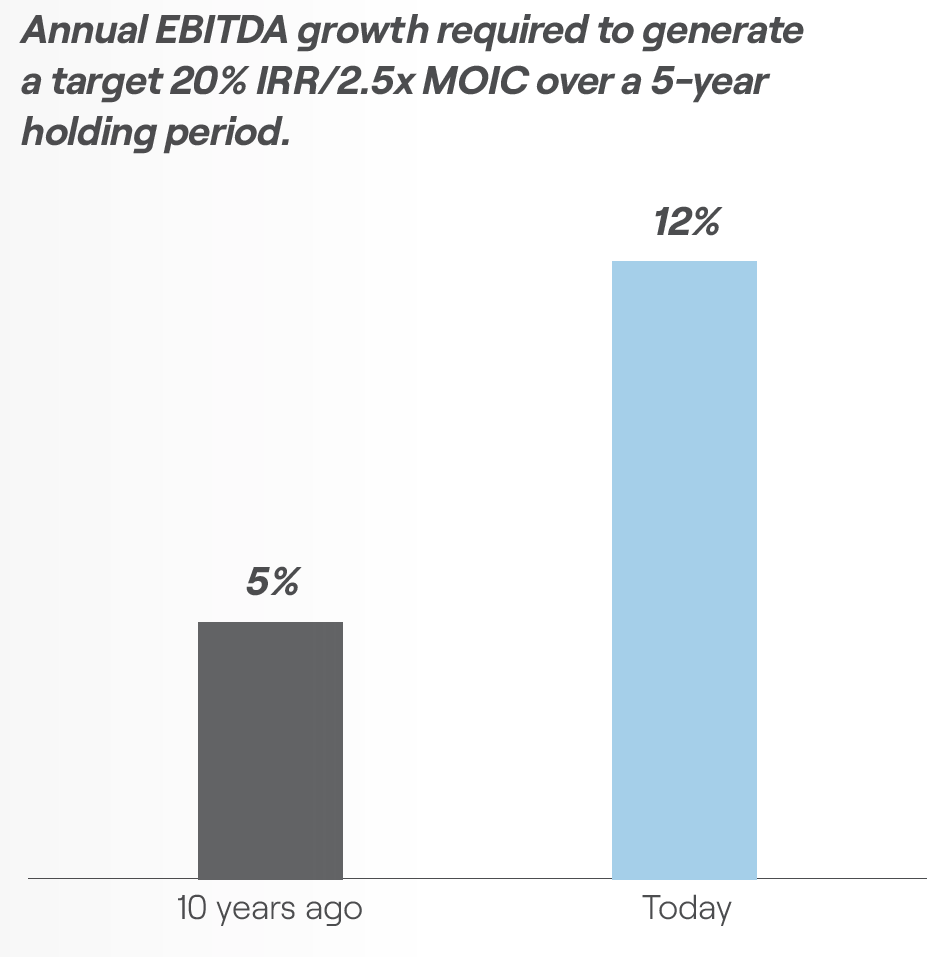

PE must ramp up company growth to achieve target returns

In 2015, buyout firms could achieve a 20% IRR and 2.5x multiple on invested capital (MOIC) by growing company EBITDA by 5% annually for five years, according to the Bain & Company Global Private Equity Report 2026.

In 2015, buyout firms could achieve a 20% IRR and 2.5x multiple on invested capital (MOIC) by growing company EBITDA by 5% annually for five years, according to the Bain & Company Global Private Equity Report 2026.

In 2025, firms needed to grow EBITDA by 12% annually for five years to reach the same return. This implies that investors have had to materially improve their value creation capabilities to reach their target returns as interest rates and pricing have increased and leverage ratios lowered.

Source: StepStone; PitchBook; Bain analysis

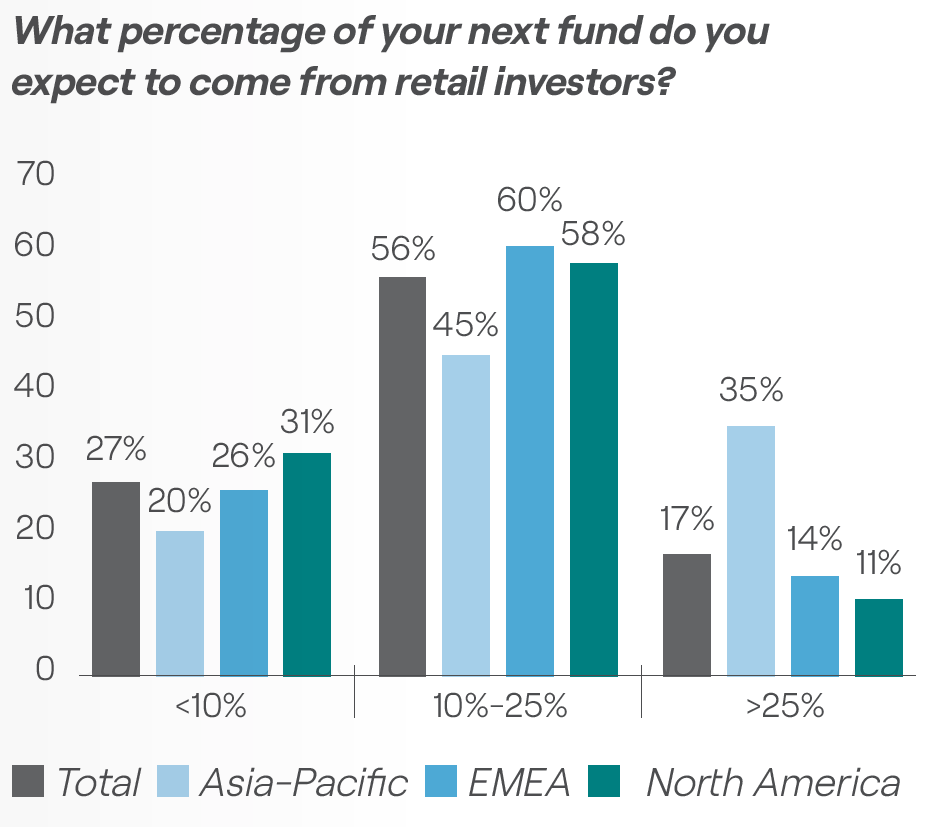

Retail investors firmly in PE’s sights

Nearly three-quarters (73%) of all respondents to the Dechert/ Mergermarket 2026 Global Private Equity Outlook expect at least 10% of capital for their next fund to come from retail investors, including 17% anticipating at least a quarter to come from them.

Nearly three-quarters (73%) of all respondents to the Dechert/ Mergermarket 2026 Global Private Equity Outlook expect at least 10% of capital for their next fund to come from retail investors, including 17% anticipating at least a quarter to come from them.

Asia-Pacific firms are particularly optimistic, with 35% expecting retail money to account for at least a quarter of heir next fund. North American firms are less so: 31% believe less than a tenth of their next fund will come from retail sources.

Source: Dechert, Mergermarket, 2026 Global Private Equity Outlook

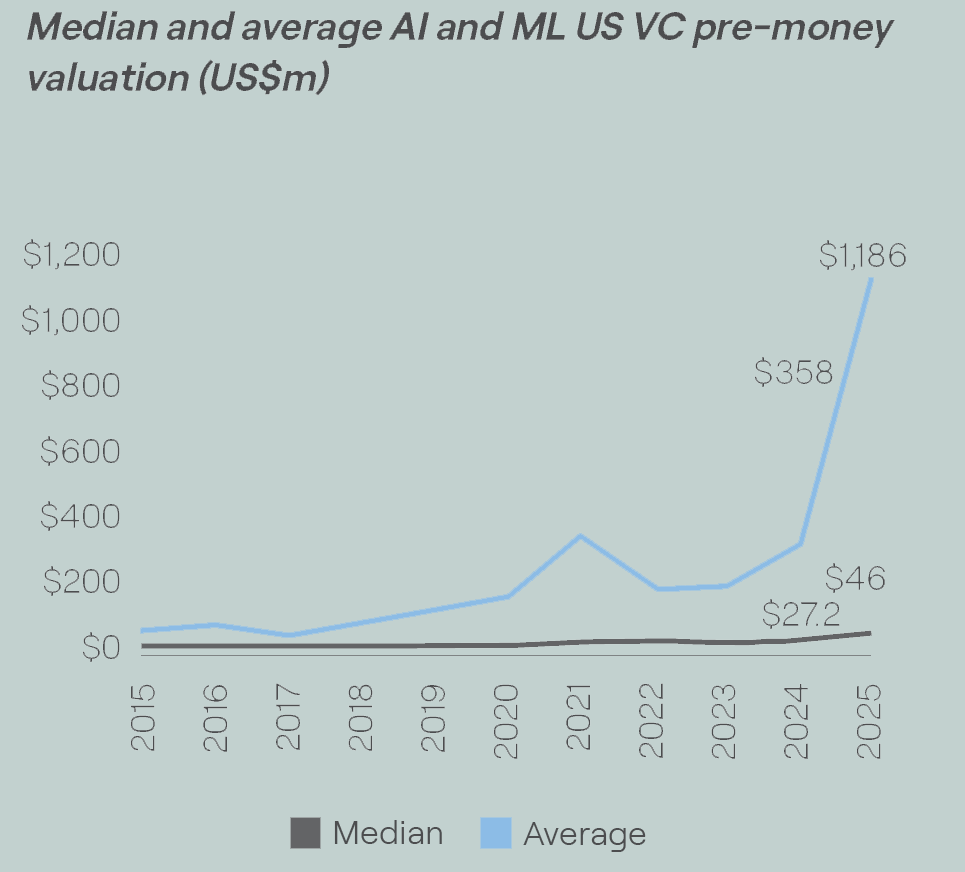

AI-related valuations skyrocket – for some

Average AI and machine learning pre-money valuations in US venture capital rose by over 230% last year, from US$358m in 2024, to US$1.19bn, according to the PitchBook-NVCA Venture Monitor for Q4 2025. However, median valuations saw lower growth, rising from US$27m to US$46m in the same period (a 70% increase).

Mega-players are driving up the averages as capital concentrates in a handful of giants, while the median figures appear to suggest more moderate valuations lower down the AL and ML segments.

Source: PitchBook-NVCA Venture Monitor

| 5% | The proportion of secondaries volume that private credit accounted for in 2023, according to Jefferies’ Global Secondaries Review, January 2024. |

| . | |

| 12% | The proportion of volume private credit accounted for in 2025, according to Jefferies’ 2026 review. Meanwhile volume in the overall secondaries market increased 114% over the same period, suggesting significant growth in private credit secondary activity. |