Fund-level reporting

Our fund-level ESG reporting continues to improve and develop. We can now provide much more information on ESG at the fund level, the portfolio GP level and at the underlying portfolio company level than was previously the case.

ESG and sustainability reputation risk

Drawing upon data received via a third-party risk platform (RepRisk), we continue to observe a lower ESG risk-profile across all our funds, notably the latest flagship fund (CIP IX).

Indeed, the combined RepRisk distribution across CIP IX indicates a strong skew to Low risk, with 91.20% of exposures classified as Low, 8.40% as Moderate, and 0.40% as High, underscoring the diversified and relatively resilient profile of the fund’s holdings.

Climate risk

For our fund-level financed (carbon) emissions we use a software platform-based solution and have migrated our data across all funds onto the new

platform over recent years. We continue to update this information periodically on at least an annual basis, and the work forms part of our wider approach to better understanding and reporting on the effect of the climate crisis across the funds, including fund level climate risk.

Our latest climate risk analysis exercise completed during 2025 also shows we continue to see a lower climate risk-profile across all our funds, notably the latest flagship fund (CIP IX).

Transition risks are concentrated in the Low and Low‑Moderate bands (Low 70.22%, Low‑Moderate 26.42%), with only small residual shares in Moderate (2.13%), Moderate‑High (1.07%), and High (0.16%).

Physical risks, by contrast, are largely Moderate (58.20%), with additional distribution across Low‑Moderate (28.58%) and Low (12.62%), and negligible exposure at the upper end (Moderate‑High 0.60%, High 0.00%), consistent with the portfolio’s sectoral and geographic mix.

Nature risk

Nature risk

Our work on nature and biodiversity continues to evolve and, in many respects, mirrors the approach we adopted to address climate change (both scenario risk analysis and measurement).

During 2025 we combined our climate-risk workstream with a more comprehensive analysis of nature-related risk across our funds. This work used the ENCORE data tool (July 2024 update) developed by Global Canopy, UNEP FI, and UNEP-WCMC to analyse a Fund’s specific dependencies and impacts related to nature.

The work highlighted a generally lower nature risk-profile across all our funds.

Enhanced data collection

Our focus from the perspective of enhanced data collection continues to be our latest flagship fund (CIP IX) and selected examples for that fund are outlined below.

Net zero:

As an indirect, pure‑play secondaries investor, the focus is on enabling and accelerating the net‑zero transition at the level of portfolio GPs rather than setting fund‑level financed targets we cannot operationally control. Our view is that the secondary market will transition in waves—first movers through 2035, a considered majority to 2055, and laggards into the 2050‑2070 window.

Within the latest flagship fund (CIP IX) specifically, approximately 29% of GPs managing assets in the fund report net‑zero commitments, and an estimated 54% of underlying companies are in countries with national net‑zero targets – evidence of a growing, if uneven, alignment landscape that supports our engagement model. To ground our stewardship, we pair portfolio‑level climate analytics with financed‑emissions measurement which we use to prioritise engagement with higher‑intensity exposures. Improving private‑markets data should further raise coverage and precision over time.

We adopt what we believe are ‘good practices‘ for secondaries where terms and visibility allow, while recognising that many net‑zero commitments remain concentrated in recent vintages that have yet to come to our market.

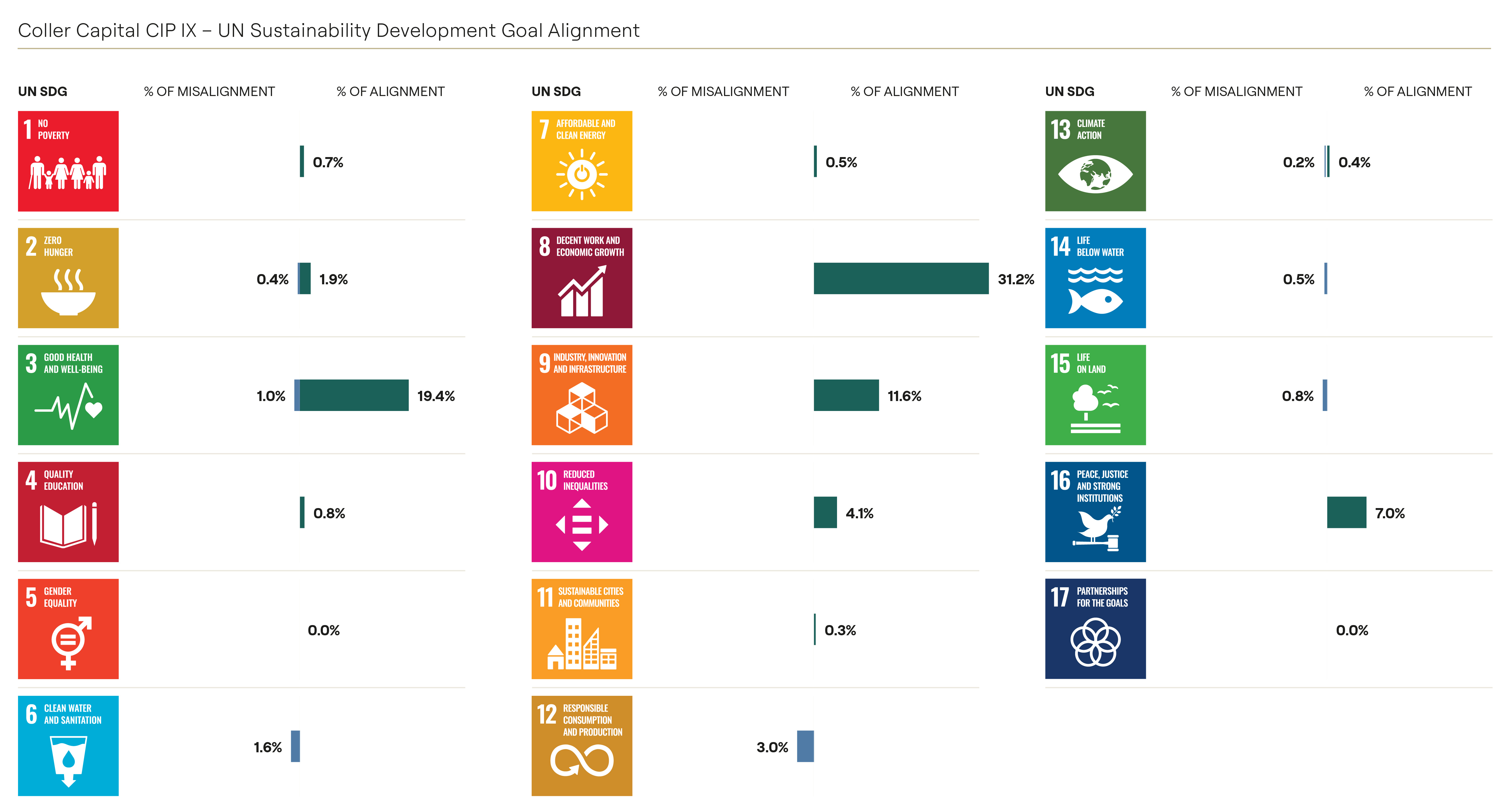

Sustainable Development Goals (SDGs):

For CIP IX, we undertook a high‑level SDG mapping to indicate where portfolio exposures are more likely to contribute positively to, or detract from, specific UN goals.

The latest breakdown shows material positive alignment to SDG 8 (Decent Work and Economic Growth), SDG 3 (Good Health and Well‑Being), SDG 9 (Industry, Innovation and Infrastructure) and SDG 16 (Peace, Justice and Strong Institutions), with modest misalignments concentrated in production and environment‑related goals (e.g., SDG 12, SDG 6, SDG 14, SDG 15).

Given our secondaries mandate and the legacy nature of many funds we acquire, the analysis is indicative and top‑down; we continue to refine coverage as GP disclosures improve and as we expand our enhanced data collection from the largest asset‑level exposures.

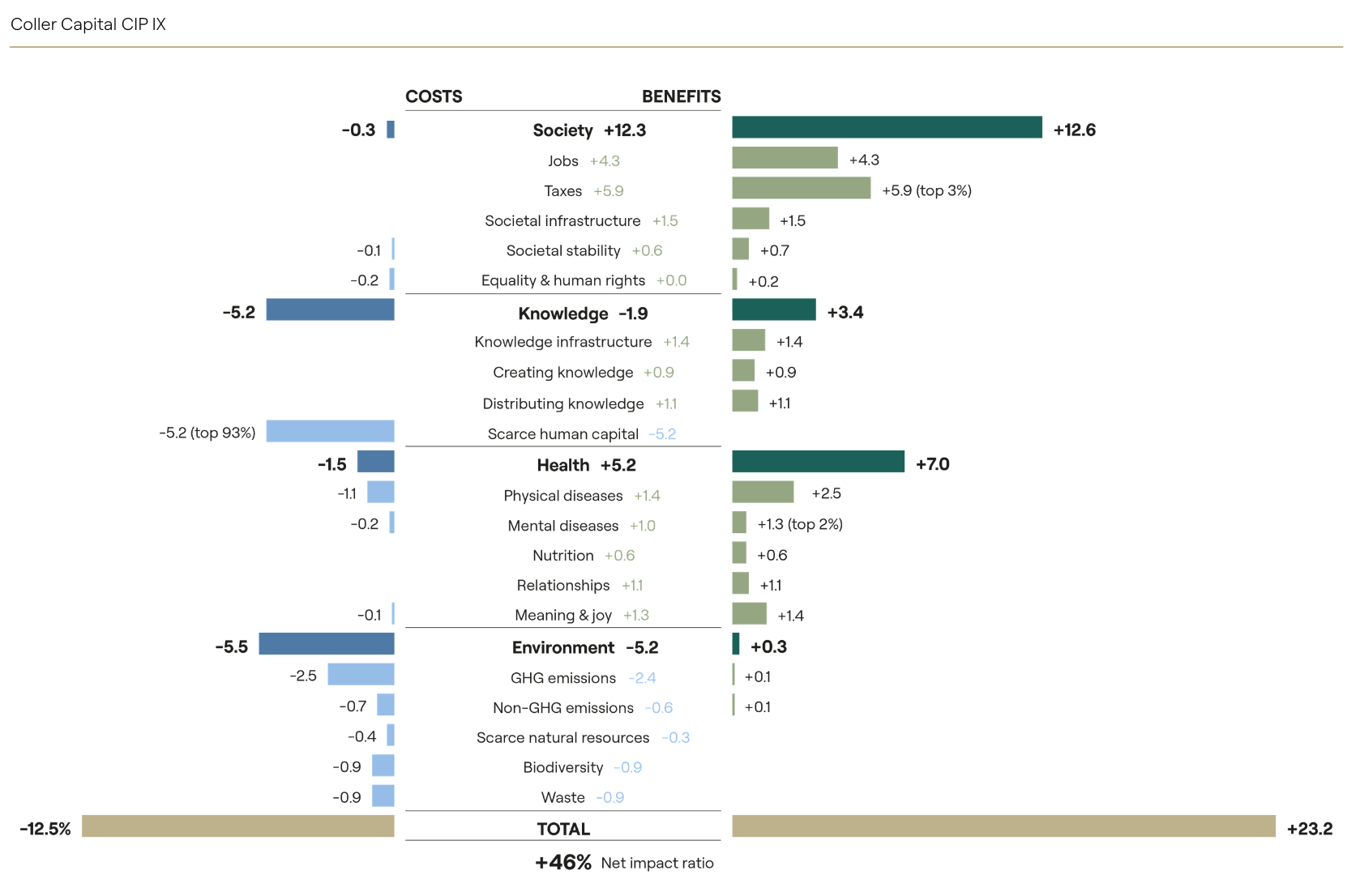

Net impact:

During 2025, we continued working with a third-party to assess the ‘net impact’ of the largest exposures in our latest equity flagship fund. This net impact measures a company’s overall positive and negative effects across various areas. Additionally, it provides all SFDR PAI (Principal Adverse Impact) indicators linked to these exposures, enhancing our overall reporting processes.